LLC Operating Agreement

Set the important rules for your LLC with our operating agreement template.

Select a state

What is an LLC operating agreement?

An LLC operating agreement is a legal document which defines the rights and duties of a limited liability company’s, or LLC’s, members; and outlines how the LLC will be owned and operated. An operating agreement formalizes the business arrangement among LLC members, clarifying roles, responsibilities, and profit-sharing. It is an essential document that all LLCs should create and keep updated.

Sometimes referred to as an LLC agreement, a written operating agreement is a key part of the LLC's business structure, providing legal protection and clarity for members. Unlike verbal agreements, which are often unenforceable and can lead to disputes, a written operating agreement is legally enforceable and helps prevent misunderstandings.

An LLC’s operating agreement governs the internal affairs and business affairs of the company, setting out management and operational responsibilities. It describes the specific functions, regulations, responsibilities, business purpose, and rules for the business, including protocols for dealing with personal or financial liabilities or internal conflicts of interest.

Create an LLC to go with your operating agreement

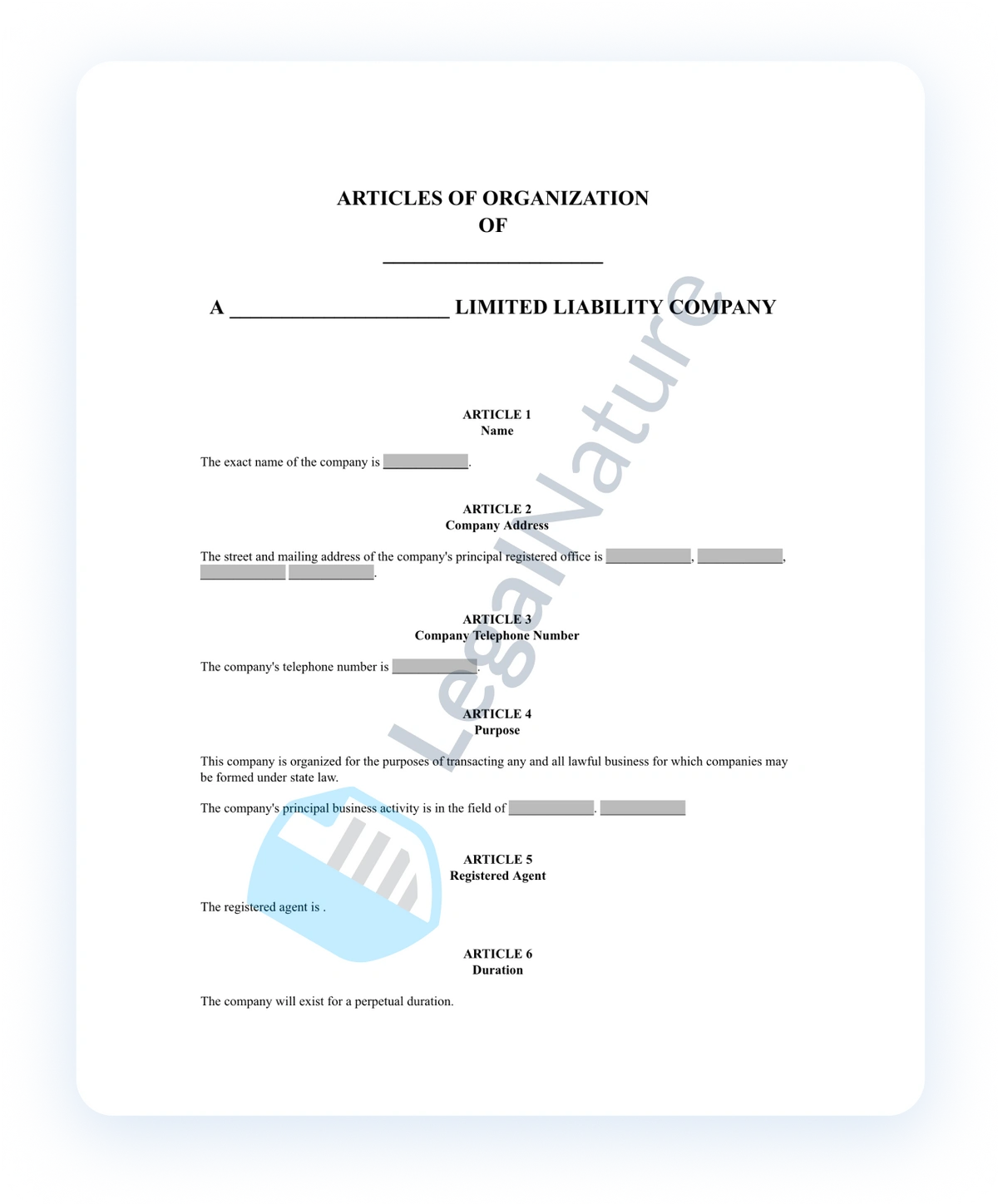

Articles of Organization Articles of Organization are filed with a State to establish an LLC. An LLC is a business entity that offers liability and tax protections to its owner.

LLC operating agreement requirements and enforecement vary by state. Select your state below to create a legally compliant document.

When to use an LLC operating agreement

While LLC operating agreements are not required by all states, they are used shortly before or after registering an LLC with a state to establish specific guidelines and operational benefits, such as:

- Asset Protection: It establishes a clear separation between the LLC and the business owners, protecting personal assets from business liabilities and distinguishing company assets. A written operating agreement also provides personal protection by helping shield personal assets from business related legal challenges.

- Customized Rules: It allows you to set specific guidelines for your business, overriding default state regulations.

- Clarity and Structure: It defines ownership percentages, profit distribution, and decision-making processes, reducing potential disputes.

- Credibility: It lends credibility to your LLC, especially important for single-member LLCs.

- Financial Flexibility: Some lenders may require an operating agreement before approving loans.

- Legal Protection: It helps maintain your LLC's limited liability status and can prevent the corporate veil from being pierced.

For LLCs with two or more members, an operating agreement is essential for outlining management rules and handling the addition of new members. Some states require operating agreements by law, and it is recommended to create your own operating agreement even if not required.

Even for single-member LLCs, an operating agreement is valuable in establishing the business as a separate entity. While you can create an operating agreement at any time, it’s best to do so when forming your LLC to ensure clear guidelines from the start.

How to create your LLC operating agreement

Gather Information

Gather all relevant information, including the LLC’s address, main business activity, member capital contributions, and agreed distribution of profits.

Answer Key Questions

Use the information you collected to complete the operating agreement. We make this easy by guiding you each step of the way and helping you to customize your document to match your specific needs. The questions and information we present to you dynamically change depending on your answers and the state selected.

Review and Sign

It is always important to read your document thoroughly to ensure it matches your needs and is free of errors and omissions. After completing the questionnaire, you can make textual changes to your document by downloading it in Microsoft Word. If no changes are needed, you can simply download the PDF version and sign.

Distribute and Store Copies

At a minimum, all parties that sign the document should receive a copy once it is fully executed (everyone has signed). Other interested parties may need or want copies as well. Be sure to store your copy in a safe location. It is a good idea to keep both a physical and electronic copy.

Why create an LLC operating agreement?

An LLC operating agreement outlines the internal regulations and specific guidelines for the operation of an LLC. Without an operating agreement a limited liability company may face several obstacles in its management and internal workings, including:

- Loss of Business Control: Without an operating agreement, your company will be governed by the state's default rules or state default rules, which may not align with the intentions of the LLC's members. A well-crafted agreement allows you to maintain control by establishing your own operational guidelines.

- Ambiguous Ownership: Lack of clear documentation can lead to confusion about each LLC member's ownership interest and member's percentage, especially during transitions like member deaths. An operating agreement provides explicit instructions for handling ownership changes, preventing potential legal disputes.

- Challenges with Member Transitions: Without defined terms, disagreements may arise when members leave the LLC. An operating agreement should detail initial contributions, ownership stakes, and document a withdrawing member's contributions, as well as the procedures for transferring a member's interest or membership interest. When a member leaves, the agreement should outline how the fair market value of their interest is determined and how it is distributed among remaining members.

- Gaps in Dispute Resolution: Multi-member LLCs often face internal conflicts. An operating agreement outlines dispute resolution procedures, potentially avoiding costly legal battles

- Vulnerability to Legal Action: The absence of an operating agreement, particularly in states requiring one, may weaken your LLC's liability protection. This could expose owners to personal liability if the business faces legal action

A well-developed LLC operating agreement serves as a crucial tool for maintaining control, clarity, and protection in your business operations.

Why choose LegalNature

LLC Operating Agreement Guide

This page explains the fundamentals of LLC operating agreements, including their purpose, key components, and general legal principles—for state-specific information about enforceability, statutory default rules, and formation requirements, refer to your state's dedicated page.

An LLC operating agreement is a business plan that defines the operational and management structure of a limited liability company. For a new business, an operating agreement is essential to clarify the business arrangement and business structure among members, ensuring everyone understands their roles, responsibilities, and how profits are distributed. Although an operating agreement is not legally required in most states, it is a good and prudent business practice to implement an operating agreement to serve as a roadmap for business operations and member relations.

LLC operating agreements may be developed before or after registering a company with the state and often contain the following key components:

Basic Company Information

- LLC name and address

- Registered agent details

- Statement of purpose

- Duration of the LLC

Membership Information

- Names and addresses of members

- Ownership percentages

- Capital contributions

- Voting rights and procedures

Management Structure

- Member managed LLC or manager managed LLC

- Roles and responsibilities of managers/members

- Decision-making processes

Financial Matters

- Distribution of profits and losses

- Tax treatment

- Accounting methods and fiscal year

Operational Procedures

- Meeting schedules and protocols

- Record-keeping requirements

- Dispute resolution methods

- Internal operations

Membership Changes

- Procedures for admitting new members

- Rules for transferring ownership interests

- Buy-sell provisions

Dissolution Procedures

- Circumstances triggering dissolution

- Asset distribution upon dissolution

It is important to maintain your limited liability company's operating agreement to make sure it is current and remains in line with the status of your company. We recommend making changes and updates under the following circumstances:

- Update as needed when significant changes occur in your business

- Obtain member approval for any amendments

- Keep all versions of the agreement on file for reference

Frequently asked questions

Why do I need an LLC operating agreement?

Every LLC needs to have an operating agreement. By laying the ground rules upfront, operating agreements go a long way to helping avoid disputes and conflict between the members later on. They help ensure that the LLC is abiding by any formal requirements under state law for operating an LLC, and they help the owners avoid taking on personal liability for the company’s debts.

What if I do not have an LLC operating agreement?

Regardless of whether they require an operating agreement, states have a set of default rules for the operation and management of businesses. Failing to create an LLC operating agreement puts your LLC at the mercy of your state’s default rules. Creating and implementing an operating agreement gives you more power and control in regard to the management of your business.

Do I need to register my LLC with the state before creating this agreement?

No. You may create and sign your operating agreement even if you have not yet officially formed it with your state. In fact, it’s often a good idea to move forward with your operating agreement ahead of time in order to finalize this important step. Our dedicated business specialists can help you quickly register your company with the state so that you can officially do business as an LLC.

LLC Operating Agreement or Articles of Organization?

These documents go hand-in-hand in the formation of a limited liability company, however there is akey distinction between the two. Articles of Organization are a document filed with a state to register and establish an LLC, while an operating agreement is the internal document defining how the business will be run.

Create your LLC operating agreement in minutes

Complete our form

;fill-opacity:1;'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M7.17816%205.46484C8.48591%205.46484%209.81742%206.23165%2011.1727%207.76529C10.8517%208.08628%2010.6467%208.28838%2010.5575%208.3716C10.4683%208.45482%2010.2514%208.6391%209.90659%208.92442C9.56182%209.20975%209.28244%209.40591%209.06844%209.51291C8.85445%209.6199%208.5721%209.73285%208.22138%209.85173C7.87067%209.97062%207.52293%2010.0301%207.17816%2010.0301C6.75017%2010.0301%206.35785%209.97656%206.00119%209.86957C5.64453%209.76257%205.28788%209.5783%204.93122%209.31675C4.57456%209.0552%204.29518%208.83229%204.09307%208.64801C3.89096%208.46374%203.58781%208.16355%203.18359%207.74745C3.95636%206.97469%204.64291%206.40107%205.24329%206.02658C5.84367%205.65209%206.48862%205.46484%207.17816%205.46484ZM7.17816%209.37024C7.61804%209.37024%207.9955%209.20975%208.31055%208.88876C8.6256%208.56776%208.78312%208.18733%208.78312%207.74745C8.78312%207.30757%208.6256%206.92714%208.31055%206.60615C7.9955%206.28516%207.61804%206.12466%207.17816%206.12466C6.73828%206.12466%206.36082%206.28516%206.04577%206.60615C5.73072%206.92714%205.5732%207.30757%205.5732%207.74745C5.5732%208.18733%205.73072%208.56776%206.04577%208.88876C6.36082%209.20975%206.73828%209.37024%207.17816%209.37024ZM7.17816%207.1768C7.17816%207.34324%207.23166%207.47996%207.33865%207.58696C7.44565%207.69395%207.58237%207.74745%207.74881%207.74745C7.8677%207.74745%207.98658%207.70584%208.10547%207.62262V7.74745C8.10547%208.009%208.01631%208.23191%207.83798%208.41619C7.65965%208.60046%207.43971%208.6926%207.17816%208.6926C6.91661%208.6926%206.69667%208.60046%206.51834%208.41619C6.34001%208.23191%206.25085%208.009%206.25085%207.74745C6.25085%207.4859%206.34001%207.26299%206.51834%207.07872C6.69667%206.89444%206.91661%206.80231%207.17816%206.80231H7.32082C7.22571%206.9212%207.17816%207.04603%207.17816%207.1768Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/svg%3e)

Preview and download your document

;fill-opacity:1;'/%3e%3cg%20clip-path='url(%23clip0_10486_8655)'%3e%3cpath%20d='M10.8931%205.49519C10.8004%205.45343%2010.6879%205.48908%2010.6427%205.57565L10.4595%205.92398L10.3128%205.85879L10.5058%205.49212L10.5069%205.48906C10.508%205.48703%2010.5091%205.48397%2010.5103%205.48194C10.54%205.4137%2010.5743%205.33324%2010.5864%205.24258C10.6239%204.97267%2010.5125%204.68749%2010.2874%204.47869C10.0733%204.28007%209.74562%204.16804%209.43445%204.18534C9.36934%204.18942%209.29984%204.20062%209.22812%204.21998C9.11446%204.25053%209.00302%204.30349%208.8982%204.37785C8.82316%204.4308%208.71833%204.52146%208.64661%204.64877L8.64551%204.65184L8.64441%204.65387L7.9603%205.95657C7.95698%205.96166%207.95369%205.96675%207.95037%205.97286C7.94705%205.97795%207.94485%205.98406%207.94265%205.99017L6.17057%209.36151C6.14408%209.41244%206.13085%209.46947%206.13305%209.5265V9.52752L6.17277%2010.6143C6.17718%2010.7202%206.22022%2010.819%206.29194%2010.8964L6.18712%2011.0919C6.14078%2011.1775%206.1794%2011.2814%206.27207%2011.3242C6.29856%2011.3364%206.32724%2011.3425%206.35483%2011.3425C6.42435%2011.3425%206.49056%2011.3069%206.52366%2011.2458L6.62516%2011.0553C6.64061%2011.0563%206.65495%2011.0573%206.6704%2011.0573C6.77412%2011.0573%206.87673%2011.0278%206.9628%2010.9687L7.91392%2010.325C7.93379%2010.3118%207.95254%2010.2955%207.96909%2010.2792C7.97241%2010.2761%207.97461%2010.2731%207.97793%2010.27C7.9989%2010.2476%208.01655%2010.2222%208.0309%2010.1957L10.1483%206.16942L10.2951%206.23461L9.35169%208.02823C9.30645%208.11379%209.34507%208.21768%209.43886%208.25943C9.46535%208.27165%209.49293%208.27674%209.52052%208.27674C9.59004%208.27674%209.65735%208.24109%209.68935%208.17896L10.7023%206.25293C10.7078%206.24581%2010.7133%206.23766%2010.7177%206.2295C10.7222%206.22134%2010.7244%206.21422%2010.7277%206.20606L10.9804%205.72533C11.0255%205.64082%2010.9858%205.53694%2010.8931%205.49519ZM6.73994%2010.6907C6.70574%2010.7131%206.6627%2010.7182%206.62408%2010.7049C6.61857%2010.7019%206.61305%2010.6988%206.60643%2010.6958C6.60312%2010.6948%206.60092%2010.6937%206.5976%2010.6927C6.5656%2010.6723%206.54575%2010.6398%206.54463%2010.6041L6.51814%209.89623C6.76641%2010.0745%207.05219%2010.2028%207.35673%2010.2741L6.73994%2010.6907Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3cpath%20d='M5.59896%2011.03C5.55151%2011.029%205.49634%2011.03%205.43897%2011.03C5.13885%2011.0331%204.57941%2011.0382%204.40067%2010.8538C4.36976%2010.8222%204.33005%2010.7652%204.3444%2010.647C4.38634%2010.314%204.58935%209.96362%204.76811%209.65499L4.79789%209.60305C4.85638%209.50221%204.91707%209.40036%204.97664%209.30056C5.14766%209.01537%205.32421%208.72%205.46433%208.40935C5.56806%208.18018%205.62542%207.96426%205.63536%207.7697C5.64859%207.50897%205.57799%207.28183%205.42571%207.09441C5.24365%206.86932%204.97774%206.70431%204.61361%206.58821C4.31128%206.49145%203.97806%206.44154%203.68455%206.39672C3.55215%206.37635%203.42635%206.35801%203.3105%206.33561C3.20899%206.31626%203.10969%206.37737%203.08982%206.47108C3.06885%206.56478%203.13505%206.65645%203.23658%206.67479C3.36015%206.69822%203.48926%206.71756%203.62497%206.73793C4.18219%206.82248%204.81444%206.91719%205.1256%207.30118C5.30986%207.52832%205.30766%207.85628%205.11788%208.2759C4.98547%208.56925%204.81444%208.85545%204.64783%209.13248C4.58825%209.23231%204.52646%209.33619%204.46687%209.43905L4.43709%209.48998C4.2418%209.82609%204.02111%2010.207%203.97146%2010.6053C3.9472%2010.7957%203.99795%2010.9567%204.12152%2011.084C4.38082%2011.3498%204.8939%2011.3763%205.29223%2011.3763C5.34408%2011.3763%205.39485%2011.3763%205.44229%2011.3753C5.49855%2011.3753%205.55043%2011.3743%205.59456%2011.3753C5.59566%2011.3753%205.59566%2011.3753%205.59676%2011.3753C5.69939%2011.3753%205.78324%2011.2989%205.78434%2011.2041C5.78544%2011.1105%205.70266%2011.031%205.59896%2011.03Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_10486_8655'%3e%3crect%20width='7.91304'%20height='7.30435'%20fill='white'%20style='fill:white;fill-opacity:1;'%20transform='translate(3.08594%204.12891)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Review and sign your document