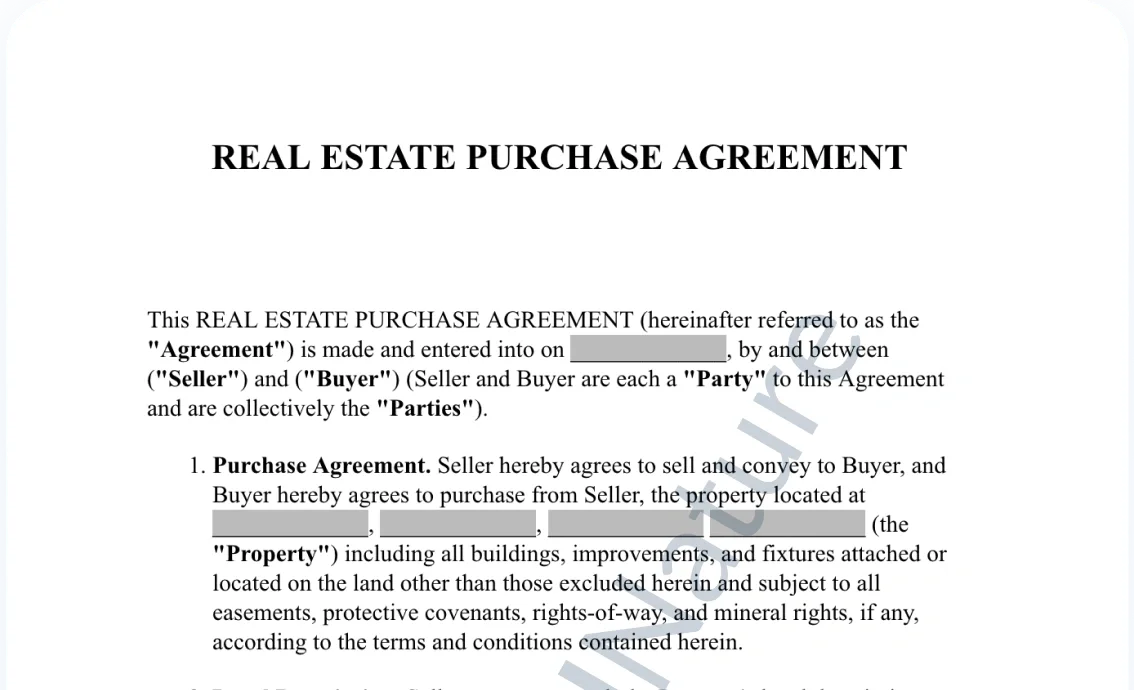

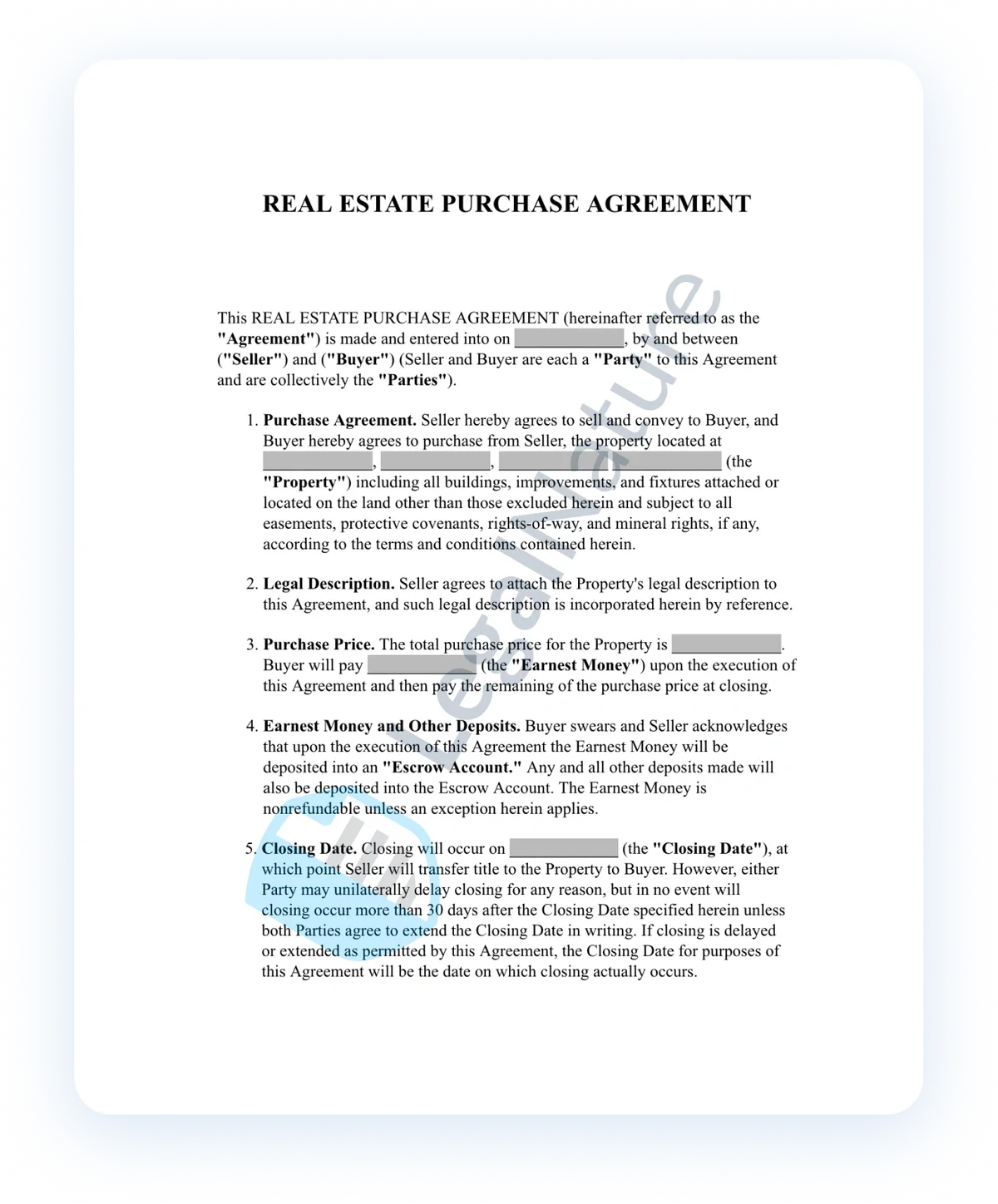

Real Estate Purchase Agreement

A real estate purchase agreement defines all the important terms in a real estate transaction between a buyer and seller. Use it to buy or sell property, a home, or even vacant land. Quickly solidify the parties’ intentions and bring the deal through to closing.

Select a state

What is a real estate purchase agreement?

A real estate purchase agreement is a legally binding contract between a buyer and seller that outlines the terms and conditions of a property sale, including the purchase price, earnest money deposit, closing date, contingencies, and specific obligations of both parties.

This critical document serves as the foundation for the entire real estate transaction, establishing the rights and responsibilities of everyone involved while protecting both the buyer’s and seller’s interests throughout the purchase process. Purchase agreements are essential documents in real estate transactions. The agreement typically includes essential details such as property description, financing terms, inspection periods, title requirements, and what fixtures or personal property will be included in the sale, as well as the effective date, which marks when the agreement becomes legally binding and contractual obligations begin. Including specific terms in the agreement is vital to ensure clarity, legal compliance, and enforceability, making it one of the most important documents in any real estate transaction.

Choose the right property transaction document for you

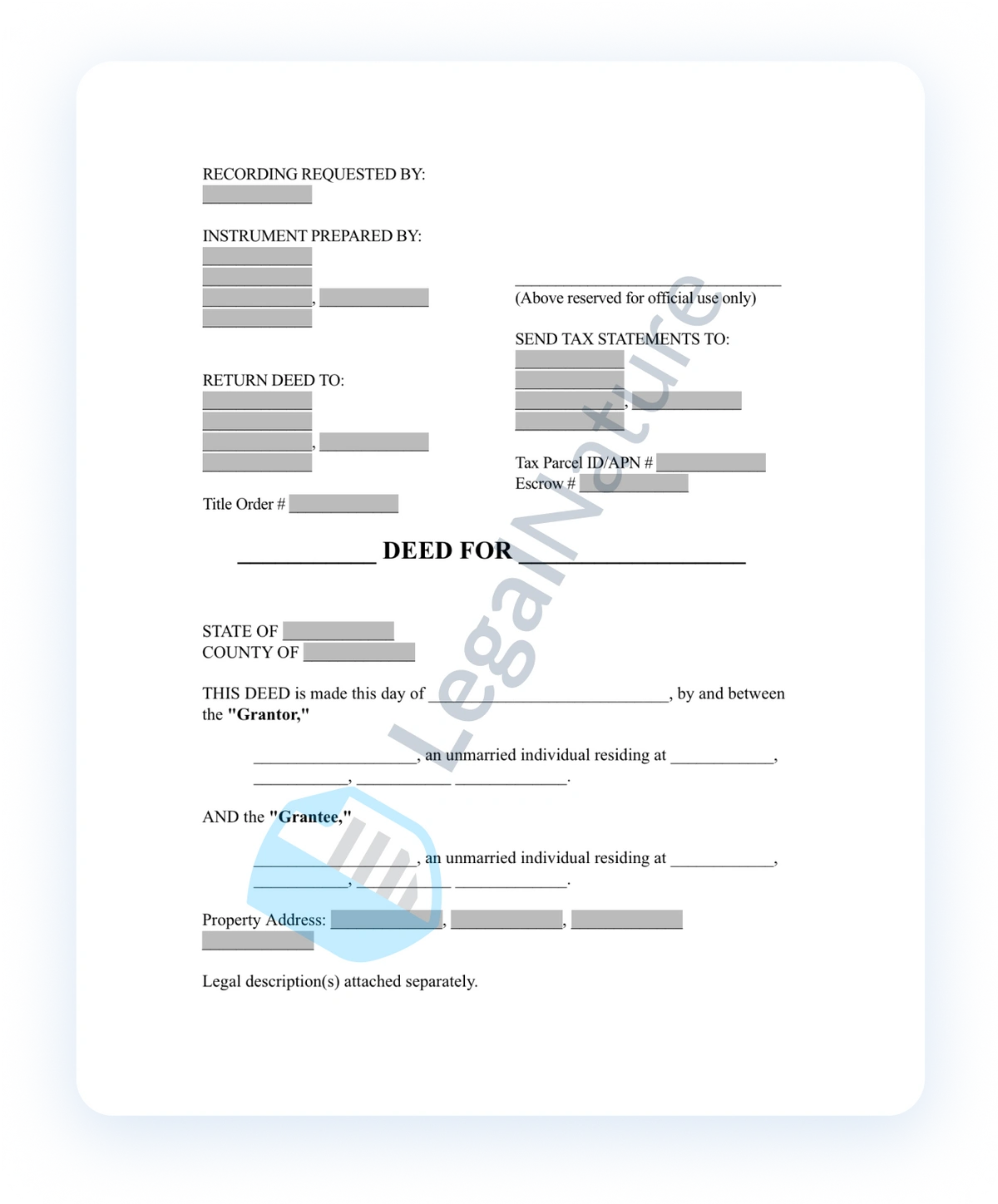

Property Deed A property deed is a legal document that officially transfers ownership of real estate from one party (the grantor) to another party (the grantee), and once properly executed, witnessed, notarized, and recorded with the county clerk's office, it provides public notice of the ownership change.

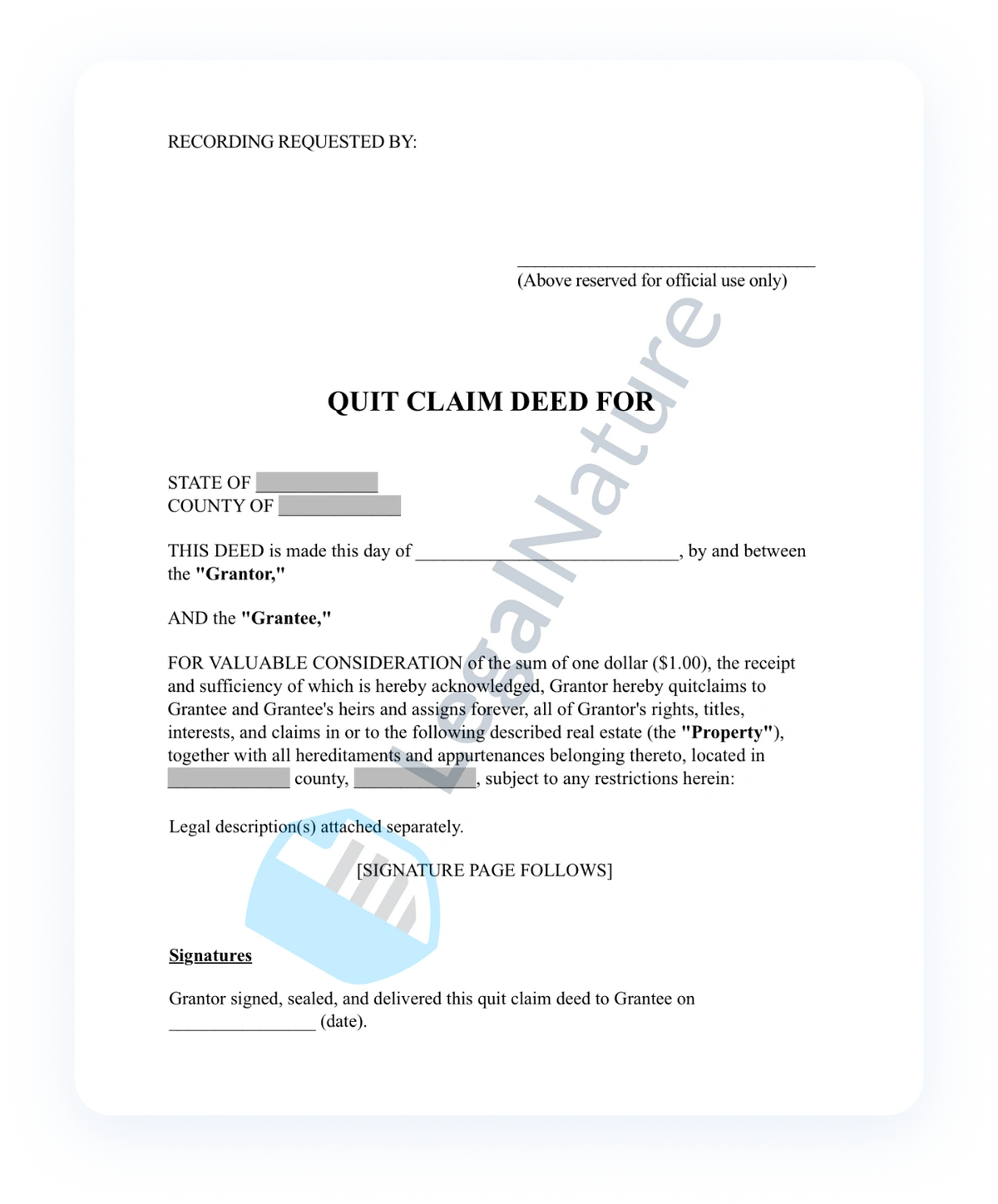

Quit Claim Deed This type of deed is commonly used for transfers between family members, adding or removing a spouse from title during divorce, correcting title issues, or transferring property into a trust, but it offers the least protection to the buyer since the grantor makes no guarantees about ownership and will not be liable if title problems arise later.

Lease Agreement A lease agreement is a legally binding contract between a landlord (lessor) and tenant (lessee) that grants the tenant the right to occupy and use a property for a specified period in exchange for regular rent payments, while establishing the rights, responsibilities, and obligations of both parties including terms for rent amount, payment schedule, security deposits, maintenance duties, and rules for property use.

Create a real estate purchase agreement in your state

When to create a real estate purchase agreement

A real estate purchase agreement should be created immediately after a buyer and seller have verbally agreed on the essential terms of a property sale—including purchase price and basic conditions—but before any money changes hands or the transaction moves forward, as this document formalizes the deal and legally protects both parties throughout the entire buying process.

The agreement is typically drafted after the buyer has viewed the property and made an offer that the seller has accepted (either as-is or after negotiations), and it must be executed before important next steps like home inspections, appraisals, title searches, and mortgage applications begin, since these contingencies and timelines are specified within the purchase agreement itself and govern how the transaction will proceed toward closing. Certain actions, such as notifying the seller of survey problems or title objections, must be completed within a specified number of business days prior to closing. If such event as a contingency not being met occurs, the agreement may be canceled or renegotiated according to the terms outlined in the contract.

Create your real estate purchase agreement in 6 easy steps

Fill out our intuitive online form

Collect the information and key points you wish to include in your real estate purchase agreement and utilize our online form to create the document. Be sure to provide buyer information, including full names and contact details, to ensure clarity in the agreement. You should also obtain the legal land description or other essential property information from county records or other sources.

Review and Sign

You should review your completed agreement in detail and make any needed edits prior to signing. While many states only require a single notary to act as a witness, you must use two witnesses for agreements concerning properties in Connecticut, Florida, Louisiana, and South Carolina. Some lenders may still require additional witnesses. Witnesses must be at least 18 years old, hold no interest in the transaction, and have no blood relation to the parties. Note that if a seller’s spouse is not also joining the agreement as a seller, then the spouse must sign an acknowledgment agreeing not to make any claim of ownership to the property after the sale.

Open Escrow

The parties will need to hire an escrow agent to manage the transaction. An escrow agent acts as a neutral third party to facilitate the buying process, including exchanging and holding funds, gathering signatures, dispersing documents, and certifying that the parties’ obligations are fulfilled.

Complete Party Obligations

Standard party obligations include providing the following items: title policy, appraisal, property inspections, seller disclosures (e.g. lead paint disclosure), property repairs and updates, required permits, and other buyer or seller contingencies (e.g. prior home sale, financing, etc.). All matters disclosed by the seller regarding the property's condition must be documented and acknowledged by the buyer. Parties may also need to obtain additional documents, such as certificates or addendums, as part of the transaction.

Close Escrow ("Closing")

During closing, the seller transfers funds to the buyer and signs over the title. Then the parties sign any remaining escrow documents. The title company will normally then record the deed at the county land recorder’s office and inform all parties when this is completed. Other documents, such as disclosures or addendums, may also be required to complete the transaction.

Move Out

The last step is for the seller to exit the property on or before the agreed move-out date. This may need to be coordinated with the buyer’s moving plans and should be started well in advance.

Why create a real estate purchase agreement?

A real estate purchase agreement is essential because it transforms a verbal understanding into a legally enforceable contract that protects both buyer and seller by clearly documenting all terms of the sale, establishing each party’s obligations, setting timelines for critical milestones, and providing legal recourse if either party fails to fulfill their commitments. A buyer's failure to meet obligations, such as securing financing or completing inspections, can result in cancellation of the agreement or loss of earnest money.

Without this binding document, buyers risk losing their earnest money deposit or having sellers back out of deals arbitrarily, while sellers have no guarantee that buyers will actually complete the purchase or secure financing. The agreement outlines the buyer's responsibilities and protections, helping to ensure that both parties are aware of their rights and obligations, and reducing the risk of financial losses, wasted time, and costly disputes that could have been prevented through clear contractual terms.

Why choose LegalNature?

The professionals at LegalNature offer the expertise and guidance to navigate the nuances of creating a real estate purchase agreement across all 50 states and the District of Columbia. LegalNature offers a 30-day money-back guarantee. If you're not happy, then we’re not happy. Give us a call and let us help.

Real estate purchase agreement help guide

A real estate purchase agreement helps you state all of the important details, including the full names of the parties, the location of the property, a clear description of the real property being sold, the purchase price, the closing date, mortgage and escrow specifications, and any other specific promises of the parties.

A strong real estate purchase agreement should include protections for the parties at every step of the way. Besides the standard clauses, the parties should be able to customize the following terms according to their preferences:

-

Whether a party is an individual, a married couple, a business entity, or a trust, as this affects how the deed transfer will proceed

-

An itemization of the personal property that the seller agrees will remain on the property and which fixtures the seller will remove before closing

-

The purchase price and earnest money deposit, including how seller credits may be applied toward the buyer's down payment or closing costs

-

The buyer’s assumption of any leases for tenants living on the property

-

The buyer’s contingencies required for the deal, including how it will be financed (third-party lending, seller financing, loan assumption, all-cash deal, or other financing), whether the property must be appraised, whether the property must be inspected, and whether the deal is contingent on the buyer first selling his or her primary residence or other property first; proceeds from the sale of a primary residence can be used for the down payment

-

Any repairs required before closing

-

Any special terms agreed to by the parties

The agreement should also specify the seller's responsibilities for disclosures and property condition. It should outline which party pays for specific expenses in the transaction, such as stating that the buyer pays earnest money, contract fees, and closing costs.

Party Details

First, you will add basic information about each party, including the names, party type, and addresses. Parties may be married individuals, unmarried individuals, businesses, or trustees.

Buyer Contingencies

Buyers will often include specific contingencies in the agreement. These are the conditions that the buyer requires to be met before closing can occur. In the event that a contingency is not met, the buyer may terminate the agreement and be refunded the earnest money and any other deposits made. However, the buyer may always choose to disregard a contingency later on if it is no longer required. The buyer always has the option to waive a contingency later on if it is no longer needed. LegalNature’s agreement includes options for adding the standard contingencies, including contingencies for receiving financing, property appraisal, inspection, and prior property sale contingencies.

A financing contingency requires that the buyer receives financing in order to close the deal. You will select the appropriate type of financing required, such as through a third-party lender, a mortgage assumption, seller financing, an all-cash transaction, or another form. A third-party lender is a traditional lending institution. A mortgage assumption is when the buyer agrees to take responsibility for the seller’s mortgage, thereby becoming liable to repay the seller’s loan. Seller financing is when the seller and buyer create a private loan contract. Lastly, all cash financing is when the buyer will finance the deal by itself. The funds do not actually need to be in the form of cash, as electronic wire transfers are normally accepted.

Under an appraisal contingency, the property must receive a professional appraisal at a value of at least the amount of the purchase price. If this does not occur, then the buyer can choose to cancel the agreement or try to renegotiate a lower purchase price. LegalNature’s agreement requires that the appraisal occur within 10 business days of signing, but you may change this if the parties agree. You will also indicate which party is responsible for covering the cost of the appraisal.

Likewise, an inspection contingency requires that a professional inspection of the property occur prior to closing. If it does not occur or if an inspector discovers a material defect, then the buyer may either cancel the agreement or require the defect to be repaired. Again, our agreement requires the inspection to happen within 10 business days of signing, but you may change this if needed.

Finally, the buyer may require that the deal is contingent on the sale of the buyer’s home or other property prior to closing.

Required Repairs

Your agreement should also indicate whether the property will need any repairs for any issues with the foundation, walls, support structures, roof, water and electrical systems, plumbing, or mechanical systems. Unless the buyer agrees otherwise, the seller will be responsible for fixing all such issues.

Executing the Agreement

To formally make the agreement effective, the parties must sign and date it in front of a notary and/or witnesses. In the majority of states, only a notary is required. You will need two witnesses to sign in Connecticut, Florida, Louisiana, and South Carolina, but you can use a notary to stand in for one of the witnesses if needed. Some lenders may still require additional witnesses. Witnesses must be at least 18 years old, hold no interest in the transaction, and have no blood relation to the parties.

State and Federal Disclosure Requirements

Federal law requires the parties to sign a lead paint disclosure statement for properties being sold that were constructed prior to 1978. LegalNature includes this disclosure with your agreement. Sellers need to store their signed copy of the disclosure for at least three years.

Frequently asked questions

Where can I find my property's legal description?

A legal description is a specific way of identifying a particular plot of real estate and the legal geographic location of its boundaries. You can find the legal description on the property's current or previously recorded deeds, your County Register or Recorder of Deeds Office (often online), property tax assessments, websites such as Zillow.com, your mortgage contract, or your land title.

The legal description is NOT the same as a property’s street address, as this may change from time to time. However, it is still recommended to include the street address on a deed, for the sake of clarity. Depending on the type of property, the legal description might be in the form of a simple lot and block reference, or it may be in a survey format giving a detailed measurement of the plot. It is crucial to get the legal description correct to complete a sale or transfer.

What does “closing” mean?

Closing is the final settlement of all the terms required in a real estate purchase agreement. This includes all contingency provisions that both parties have included, the documents that need to be exchanged, and any sums of money that need to be paid.

What is a contingency?

In terms of a real estate purchase agreement, a contingency is a contractual requirement that must be completed in order for the purchase to be completed. Contingencies are added as terms to the written purchase contract that both the buyer and seller agree to. Common contingencies include the following:

- Clear title

- Buyer's mortgage approval

- House inspection

- Sale of current property

- Lead-based paint inspection

- Homeowners' Association (HOA) documents

What is an encroachment?

In the context of real estate, an encroachment is a type of encumbrance characterized by a physical intrusion on a property owner's land. An example of an encroachment is when a person constructs a structure that extends beyond the boundaries of his or her property and onto, over, or underneath the neighboring property. Here, the person is said to be "encroaching" on the neighbor's property.

What is escrow?

Escrow is an arrangement where a third party holds funds and manages payments. Escrow arrangements are normally enforced when large sums of money change hands, such as real estate purchases. The third-party will safeguard funds until the terms of a contract are fulfilled. This way, the two contracting parties are kept safe without needing to transfer money to each other.

Create your real estate purchase agreement in minutes

Complete our form

;fill-opacity:1;'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M7.17816%205.46484C8.48591%205.46484%209.81742%206.23165%2011.1727%207.76529C10.8517%208.08628%2010.6467%208.28838%2010.5575%208.3716C10.4683%208.45482%2010.2514%208.6391%209.90659%208.92442C9.56182%209.20975%209.28244%209.40591%209.06844%209.51291C8.85445%209.6199%208.5721%209.73285%208.22138%209.85173C7.87067%209.97062%207.52293%2010.0301%207.17816%2010.0301C6.75017%2010.0301%206.35785%209.97656%206.00119%209.86957C5.64453%209.76257%205.28788%209.5783%204.93122%209.31675C4.57456%209.0552%204.29518%208.83229%204.09307%208.64801C3.89096%208.46374%203.58781%208.16355%203.18359%207.74745C3.95636%206.97469%204.64291%206.40107%205.24329%206.02658C5.84367%205.65209%206.48862%205.46484%207.17816%205.46484ZM7.17816%209.37024C7.61804%209.37024%207.9955%209.20975%208.31055%208.88876C8.6256%208.56776%208.78312%208.18733%208.78312%207.74745C8.78312%207.30757%208.6256%206.92714%208.31055%206.60615C7.9955%206.28516%207.61804%206.12466%207.17816%206.12466C6.73828%206.12466%206.36082%206.28516%206.04577%206.60615C5.73072%206.92714%205.5732%207.30757%205.5732%207.74745C5.5732%208.18733%205.73072%208.56776%206.04577%208.88876C6.36082%209.20975%206.73828%209.37024%207.17816%209.37024ZM7.17816%207.1768C7.17816%207.34324%207.23166%207.47996%207.33865%207.58696C7.44565%207.69395%207.58237%207.74745%207.74881%207.74745C7.8677%207.74745%207.98658%207.70584%208.10547%207.62262V7.74745C8.10547%208.009%208.01631%208.23191%207.83798%208.41619C7.65965%208.60046%207.43971%208.6926%207.17816%208.6926C6.91661%208.6926%206.69667%208.60046%206.51834%208.41619C6.34001%208.23191%206.25085%208.009%206.25085%207.74745C6.25085%207.4859%206.34001%207.26299%206.51834%207.07872C6.69667%206.89444%206.91661%206.80231%207.17816%206.80231H7.32082C7.22571%206.9212%207.17816%207.04603%207.17816%207.1768Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/svg%3e)

Preview and download your document

;fill-opacity:1;'/%3e%3cg%20clip-path='url(%23clip0_10486_8655)'%3e%3cpath%20d='M10.8931%205.49519C10.8004%205.45343%2010.6879%205.48908%2010.6427%205.57565L10.4595%205.92398L10.3128%205.85879L10.5058%205.49212L10.5069%205.48906C10.508%205.48703%2010.5091%205.48397%2010.5103%205.48194C10.54%205.4137%2010.5743%205.33324%2010.5864%205.24258C10.6239%204.97267%2010.5125%204.68749%2010.2874%204.47869C10.0733%204.28007%209.74562%204.16804%209.43445%204.18534C9.36934%204.18942%209.29984%204.20062%209.22812%204.21998C9.11446%204.25053%209.00302%204.30349%208.8982%204.37785C8.82316%204.4308%208.71833%204.52146%208.64661%204.64877L8.64551%204.65184L8.64441%204.65387L7.9603%205.95657C7.95698%205.96166%207.95369%205.96675%207.95037%205.97286C7.94705%205.97795%207.94485%205.98406%207.94265%205.99017L6.17057%209.36151C6.14408%209.41244%206.13085%209.46947%206.13305%209.5265V9.52752L6.17277%2010.6143C6.17718%2010.7202%206.22022%2010.819%206.29194%2010.8964L6.18712%2011.0919C6.14078%2011.1775%206.1794%2011.2814%206.27207%2011.3242C6.29856%2011.3364%206.32724%2011.3425%206.35483%2011.3425C6.42435%2011.3425%206.49056%2011.3069%206.52366%2011.2458L6.62516%2011.0553C6.64061%2011.0563%206.65495%2011.0573%206.6704%2011.0573C6.77412%2011.0573%206.87673%2011.0278%206.9628%2010.9687L7.91392%2010.325C7.93379%2010.3118%207.95254%2010.2955%207.96909%2010.2792C7.97241%2010.2761%207.97461%2010.2731%207.97793%2010.27C7.9989%2010.2476%208.01655%2010.2222%208.0309%2010.1957L10.1483%206.16942L10.2951%206.23461L9.35169%208.02823C9.30645%208.11379%209.34507%208.21768%209.43886%208.25943C9.46535%208.27165%209.49293%208.27674%209.52052%208.27674C9.59004%208.27674%209.65735%208.24109%209.68935%208.17896L10.7023%206.25293C10.7078%206.24581%2010.7133%206.23766%2010.7177%206.2295C10.7222%206.22134%2010.7244%206.21422%2010.7277%206.20606L10.9804%205.72533C11.0255%205.64082%2010.9858%205.53694%2010.8931%205.49519ZM6.73994%2010.6907C6.70574%2010.7131%206.6627%2010.7182%206.62408%2010.7049C6.61857%2010.7019%206.61305%2010.6988%206.60643%2010.6958C6.60312%2010.6948%206.60092%2010.6937%206.5976%2010.6927C6.5656%2010.6723%206.54575%2010.6398%206.54463%2010.6041L6.51814%209.89623C6.76641%2010.0745%207.05219%2010.2028%207.35673%2010.2741L6.73994%2010.6907Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3cpath%20d='M5.59896%2011.03C5.55151%2011.029%205.49634%2011.03%205.43897%2011.03C5.13885%2011.0331%204.57941%2011.0382%204.40067%2010.8538C4.36976%2010.8222%204.33005%2010.7652%204.3444%2010.647C4.38634%2010.314%204.58935%209.96362%204.76811%209.65499L4.79789%209.60305C4.85638%209.50221%204.91707%209.40036%204.97664%209.30056C5.14766%209.01537%205.32421%208.72%205.46433%208.40935C5.56806%208.18018%205.62542%207.96426%205.63536%207.7697C5.64859%207.50897%205.57799%207.28183%205.42571%207.09441C5.24365%206.86932%204.97774%206.70431%204.61361%206.58821C4.31128%206.49145%203.97806%206.44154%203.68455%206.39672C3.55215%206.37635%203.42635%206.35801%203.3105%206.33561C3.20899%206.31626%203.10969%206.37737%203.08982%206.47108C3.06885%206.56478%203.13505%206.65645%203.23658%206.67479C3.36015%206.69822%203.48926%206.71756%203.62497%206.73793C4.18219%206.82248%204.81444%206.91719%205.1256%207.30118C5.30986%207.52832%205.30766%207.85628%205.11788%208.2759C4.98547%208.56925%204.81444%208.85545%204.64783%209.13248C4.58825%209.23231%204.52646%209.33619%204.46687%209.43905L4.43709%209.48998C4.2418%209.82609%204.02111%2010.207%203.97146%2010.6053C3.9472%2010.7957%203.99795%2010.9567%204.12152%2011.084C4.38082%2011.3498%204.8939%2011.3763%205.29223%2011.3763C5.34408%2011.3763%205.39485%2011.3763%205.44229%2011.3753C5.49855%2011.3753%205.55043%2011.3743%205.59456%2011.3753C5.59566%2011.3753%205.59566%2011.3753%205.59676%2011.3753C5.69939%2011.3753%205.78324%2011.2989%205.78434%2011.2041C5.78544%2011.1105%205.70266%2011.031%205.59896%2011.03Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_10486_8655'%3e%3crect%20width='7.91304'%20height='7.30435'%20fill='white'%20style='fill:white;fill-opacity:1;'%20transform='translate(3.08594%204.12891)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Review and sign your document